SDLT is not a simple tax. HMRC says so. The courts say so. The statutory framework says so. And 12,737 real matters handled by Compass say so. Yet still some market commentators state otherwise, so here is what the law, the data, and the regulatory framework tell us.

The legal position is not ambiguous

HMRC has confirmed explicitly that filing SDLT returns constitutes tax advice requiring registration under the new regime. That is not Compass’s interpretation. It is HMRC’s published position. The courts have been equally clear. In Hurlingham Estates v Wilde and Partners, the court established that a solicitor handling a property transaction owes a duty to advise on its tax implications, or to direct the client to someone who can. In Lewis v Cunningtons, decided in 2023, a firm whose disclaimer purported to exclude that duty was ordered to pay £400,000 in damages. The disclaimer did not work. It never does, because the Consumer Rights Act 2015 provides that the implied term of reasonable care and skill in consumer services cannot be excluded by contract.

What 12,737 matters show

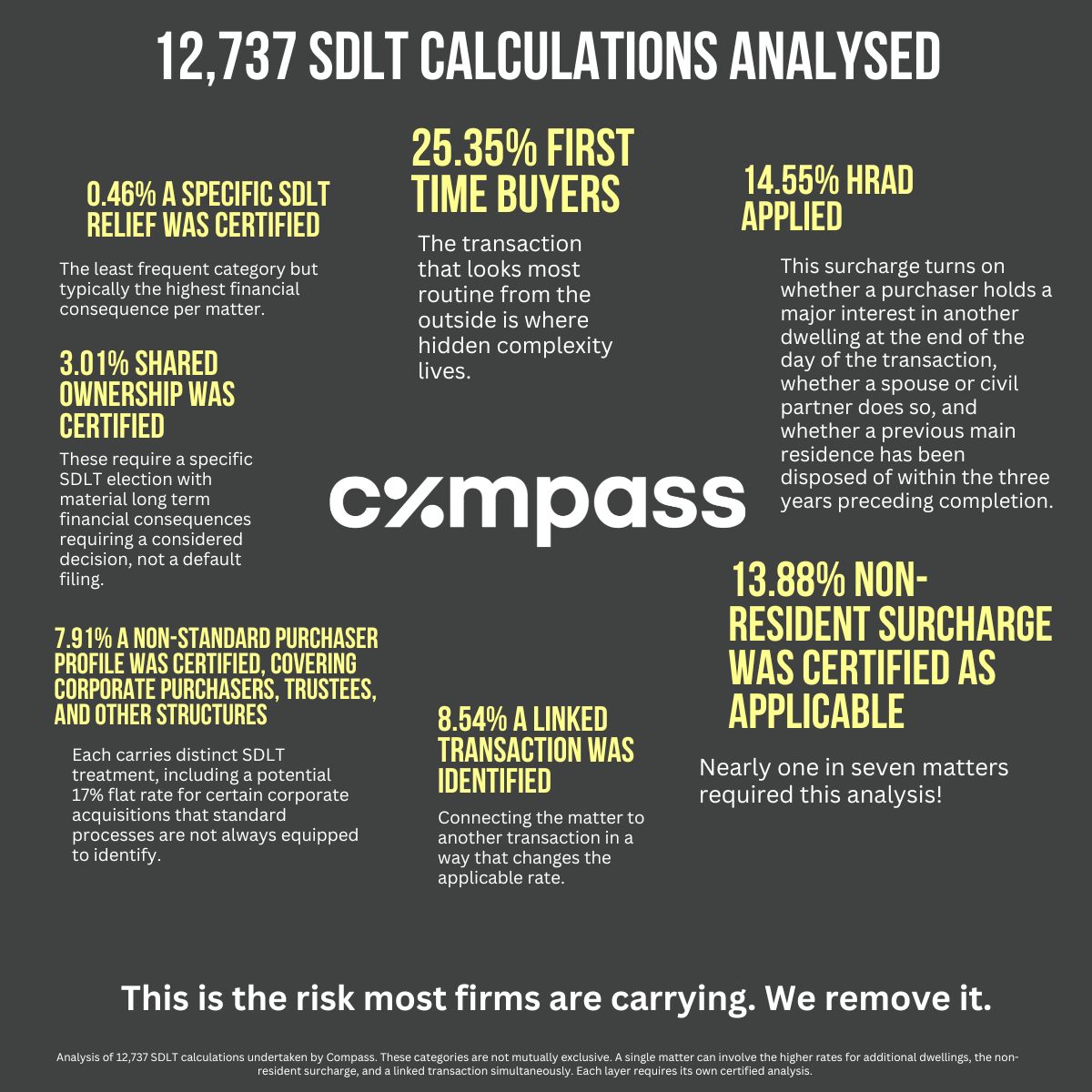

Every figure below is a certified outcome on a real matter, taken from 12,737 matters processed through the Compass platform.

In 25.35% of matters, first time buyer relief was certified as applicable. The transaction that looks most routine from the outside is precisely where hidden complexity lives. FTB relief requires that neither the purchaser nor any joint purchaser has previously owned a dwelling anywhere in the world. The client who inherited a share of a property thirty years ago, sold it, and has not thought about it since does not consider themselves anything other than a first time buyer. They are not. The relief also carries a price cap. Applying it above the threshold is a certified error.

In 14.55% of matters, the higher rates for additional dwellings were certified as applicable. This surcharge turns on whether a purchaser holds a major interest in another dwelling at the end of the day of the transaction, whether a spouse or civil partner does so, and whether a previous main residence has been disposed of within the three years preceding completion. A purchaser who owns a property abroad, whose spouse retained a property from a previous relationship, or who sold a previous main residence twenty months ago rather than thirty-seven, may not realise any of those facts matter.

In 13.88% of matters, the non-resident surcharge was certified as applicable. For individuals this turns on a specific statutory residence test applied to the twelve months preceding completion. For companies the analysis follows corporation tax residence rules. For joint purchasers, the surcharge applies if any one of them is non-resident. None of these tests is intuitive and none is something a standard questionnaire reliably identifies. Nearly one in seven matters required this analysis.

In 8.54% of matters, a linked transaction was certified, connecting the matter to another transaction in a way that changes the applicable rate. In 7.91% of matters, a non-standard purchaser profile was certified, covering corporate purchasers, trustees, and other structures each carrying distinct SDLT treatment, including a potential 17% flat rate for certain corporate acquisitions that standard processes are not always equipped to identify.

In 3.01% of matters, shared ownership tenure was certified, carrying a specific SDLT election with material long term financial consequences requiring a considered decision, not a default filing. In 0.46% of matters, a specific SDLT relief was certified, the least frequent category but typically the highest financial consequence per matter.

These categories are not mutually exclusive. A single matter can involve the higher rates for additional dwellings, the non-resident surcharge, and a linked transaction simultaneously. Each layer requires its own certified analysis.

A matter of routine?

To conclude that a transaction is routine, a conveyancer must already apply SDLT knowledge to the specific facts of that matter. They must consider ownership history, linked transactions, purchaser profile, applicable reliefs and surcharges. They must reach a professional conclusion on each question. That process is tax advice. Under Clause 1 of Finance Bill 2026, it is the provision of assistance in relation to tax, including assistance with a document HMRC will rely on to determine the client’s tax position.

Conveyancers are specialists. Property law, client care, transaction management, the coordination of an impossibly complex process under enormous time pressure. That specialism is what clients rely on and what conveyancers consistently deliver. Nobody reading this should take from it that conveyancers are anything other than skilled professionals operating in a demanding environment.

But specialism cuts both ways. SDLT has become a tax that requires its own specialism. Not because conveyancers are incapable, but because the legislation has evolved to a point where getting it right consistently, on every matter, requires dedicated focus, dedicated systems, and dedicated professional accountability. Systems that are dynamic, not fixed. That respond to the transaction, not to assumptions about it.

So, the question is not whether you are competent. You are. The question is whether the time spent on submissions, questionnaires, second reviews, and keeping pace with a tax that changes constantly, is time better placed elsewhere.

None of this is new. The argument that conveyancers performing SDLT calculations and submissions are providing tax advice has been made consistently, in case law, in regulatory guidance, and in professional commentary, for years. The new registration regime is not a new idea. It is the latest in a long line of signals from courts, regulators, and now Parliament, all pointing in the same direction. The question is no longer whether SDLT handling carries professional and legal weight. It always did. The question is whether your firm is the right place for that weight to sit.

Click here to book a no obligation meeting to find out more about the Compass platform